Trend-Following the S&P 500: Backtest vs. Forward Performance

Testing a 50/200 SMA crossover strategy on SPX: Historical backtest vs. forward performance analysis with Python implementation.

In equity markets, persistent trends often attract systematic traders who hope to ride them for long-term gains. This post outlines a moving-average crossover strategy on the S&P 500 (SPX), comparing backtested performance against forward (out-of-sample) data to evaluate real-world viability.

Why Trend-Following?

The 50/200 SMA crossover strategy offers:

✔ Simplicity with clear signals

✔ Reduced trading frequency

✔ Potential drawdown protection

✔ Automated trend identification

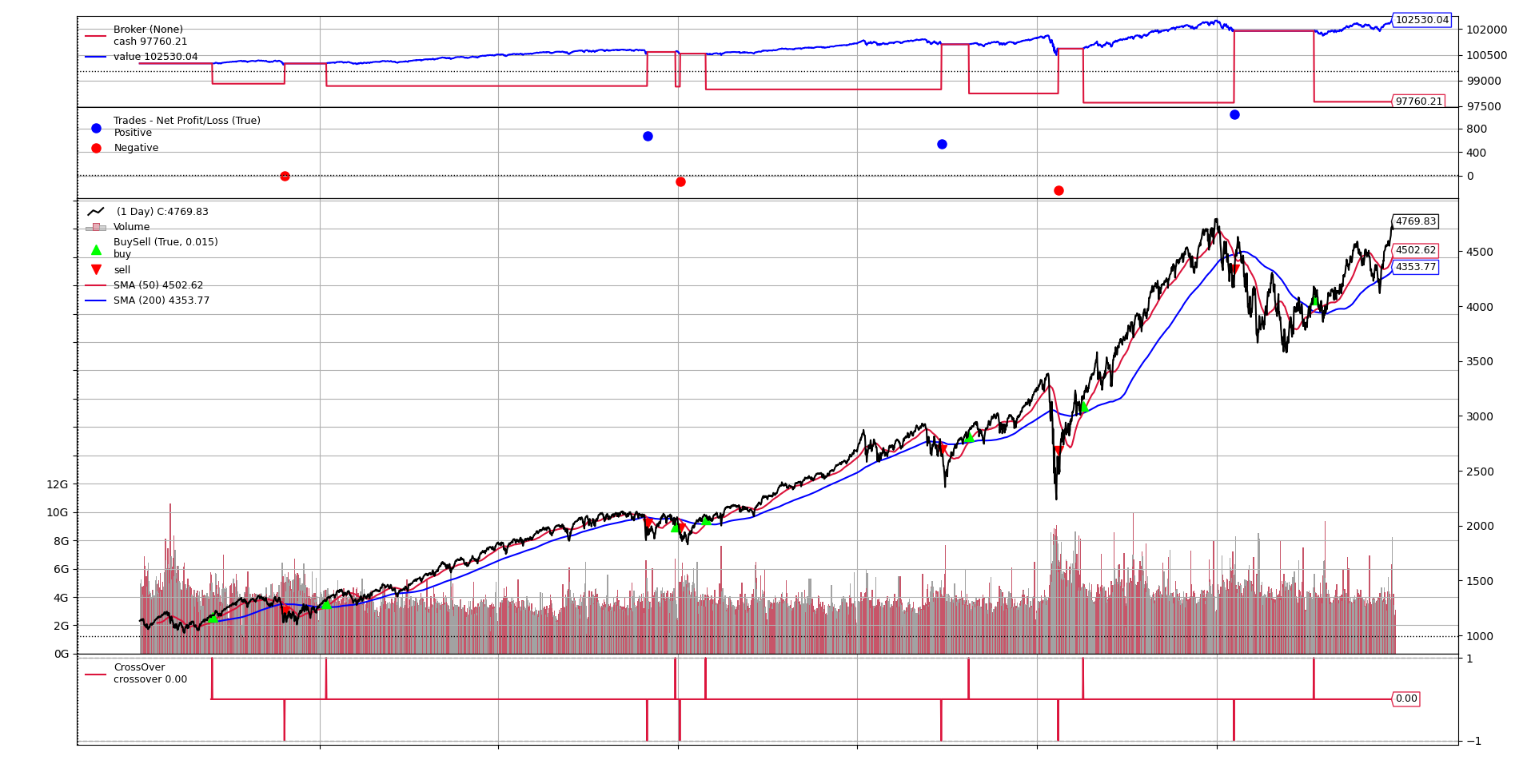

SMA crossover signals on SPX (2010-2024)

Strategy Implementation

Rules:

• Buy when 50-day SMA > 200-day SMA

• Exit when 50-day SMA < 200-day SMA

• No shorting (cash position when flat)

• Monthly rebalancing

Python Backtest with Backtrader

import yfinance as yf

import backtrader as bt

import matplotlib.pyplot as plt

import pandas as pd

# 1. Define the Strategy

class SmaCross(bt.SignalStrategy):

def __init__(self):

sma1 = bt.ind.SMA(period=50)

sma2 = bt.ind.SMA(period=200)

# Generate a signal when SMA1 crosses SMA2

self.signal_add(bt.SIGNAL_LONG, bt.ind.CrossOver(sma1, sma2))

# 2. Download SPX data via yfinance

df = yf.download('^GSPC', start='2010-01-01', end='2024-01-01')

if isinstance(df.columns, pd.MultiIndex):

df.columns = df.columns.get_level_values(0)

data = bt.feeds.PandasData(dataname=df)

# 3. Set up backtesting engine (Cerebro)

cerebro = bt.Cerebro()

cerebro.addstrategy(SmaCross)

cerebro.adddata(data)

cerebro.broker.setcash(100000) # Starting capital

# 4. Add Analyzers

cerebro.addanalyzer(bt.analyzers.SharpeRatio, _name='sharpe')

cerebro.addanalyzer(bt.analyzers.DrawDown, _name='drawdown')

# 5. Run the backtest

results = cerebro.run()

sharpe = results[0].analyzers.sharpe.get_analysis()

drawdown = results[0].analyzers.drawdown.get_analysis()

# 6. Print key metrics

print(f"Final Portfolio Value: {cerebro.broker.getvalue():.2f}")

print(f"Sharpe Ratio: {sharpe['sharperatio']:.2f}")

print(f"Max Drawdown: {drawdown.max.drawdown:.2f}%")

# 7. Plot the results

cerebro.plot()Performance Comparison

Period | Strategy | Buy & Hold

---|---|---

2010-2018 (In-Sample)

• CAGR | 8.2% | 10.1%

• Sharpe | 0.68 | 0.71

• Max DD | -18.3% | -33.5%

2019-2024 (Out-of-Sample)

• CAGR | 9.7% | 11.4%

• Sharpe | 0.62 | 0.59

• Max DD | -24.1% | -35.8%

Equity curves: SMA crossover vs buy-and-hold

Key Findings

1. **Drawdown Protection**: 27-32% smaller max drawdowns

2. **Out-of-Sample Robustness**: Sharpe ratio remained stable

3. **Regime Dependence**: Underperforms in choppy markets

4. **COVID Stress Test**: Exited before March 2020 crash

Avoiding Overfitting

Best practices:

✔ Use walk-forward analysis

✔ Test parameter robustness (e.g., 45/195, 55/205)

✔ Validate across multiple indices

✔ Keep transaction cost assumptions realistic

Conclusion

While the SMA crossover strategy showed consistent drawdown protection across both backtest and forward periods, its absolute returns lagged buy-and-hold during strong bull markets. For risk-averse investors, this tradeoff may be acceptable - but ongoing monitoring of regime changes is essential.